P&G Announces Fiscal Year 2021 First Quarter Results

Net Sales +9%; Organic Sales +9%; Diluted Net EPS $1.63, +20% vs. prior year Reported EPS; +19% vs. prior year Core EPS UPDATES GAAP EPS GUIDANCE TO REFLECT DEBT RESTRUCTURING; RAISES SALES, CORE EPS, ADJUSTED FREE CASH FLOW PRODUCTIVITY AND CASH RETURN GUIDANCE

The Procter & Gamble Company (NYSE:PG) reported first quarter fiscal year 2021 net sales of $19.3 billion, an increase of nine percent versus the prior year. Excluding the net impacts of foreign exchange, acquisitions and divestitures, organic sales also increased nine percent. Diluted net earnings per share were $1.63, an increase of 20% versus the prior year reported EPS and an increase of 19% versus the prior year Core EPS. On a currency-neutral basis, EPS increased 22% versus the prior year core results.

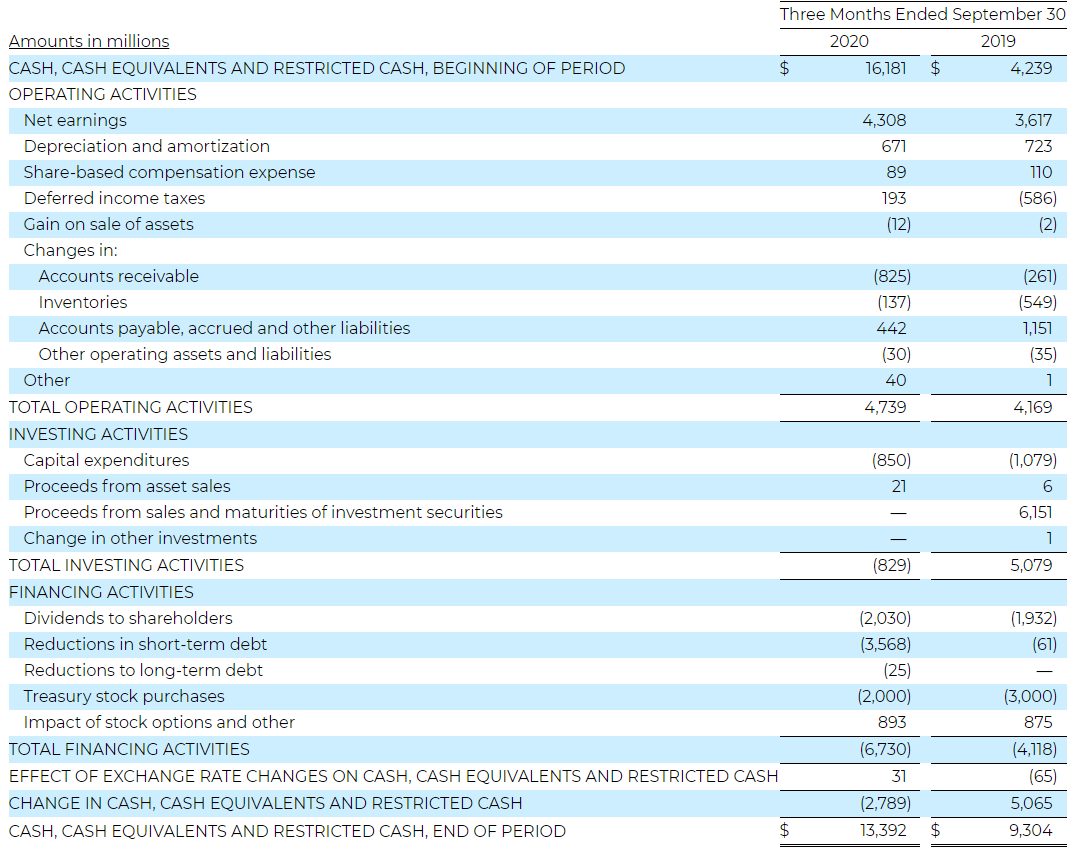

Operating cash flow was $4.7 billion for the quarter. Adjusted free cash flow productivity was 95%. The Company returned $4 billion of cash to shareholders via $2 billion of dividend payments and $2 billion of common stock repurchases.

“We delivered another strong quarter of organic sales growth, core earnings per share and cash returned to shareowners, enabling us to increase our outlook for fiscal year results,” said David Taylor, Chairman, President and Chief Executive Officer. “Our near-term priorities continue to be employee health and safety, maximizing availability of P&G products for consumers around the world, and helping society meet the challenges of the COVID crisis. We remain firmly focused on executing our strategies of superiority, productivity, constructive disruption and improving P&G’s organization and culture to deliver balanced top-line and bottom-line growth along with strong cash generation.”

July – September Quarter Discussion

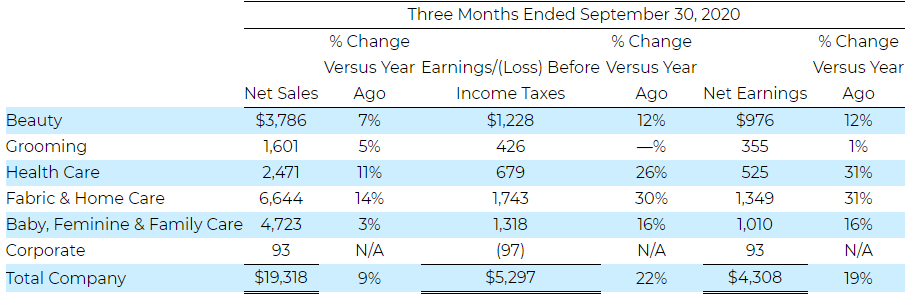

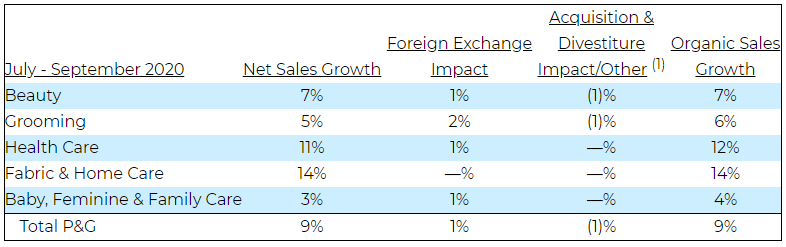

Net sales in the first quarter of fiscal year 2021 were $19.3 billion, a nine percent increase versus the prior year. Unfavorable foreign exchange negatively impacted sales by one percentage point for the quarter. Excluding the impacts of foreign exchange, acquisitions and divestitures, organic sales also increased nine percent, driven by a seven percent increase in organic shipment volume, one percentage point of increased pricing and one percentage point of positive mix impact. Positive mix was driven by the disproportionate growth of premium home, health and hygiene products and the North American business, driven in part by pandemic-related consumption and inventory increases.

[table id=1 /]

(1)Net sales percentage changes are approximations based on quantitative formulas that are consistently applied.

(2)Other includes the sales mix impact from acquisitions and divestitures and rounding impacts necessary to reconcile volume to net sales.

- Beauty segment organic sales increased seven percent versus year ago. Skin and Personal Care organic sales increased high single digits driven by innovation-led growth in North America and Greater China. North America Skin and Personal Care grew mid-teens behind the launch of Safeguard hand soap and hand sanitizer and premium innovations on Olay. Globally, Personal Cleansing grew over 30%, with double digit growth in every region. Greater China SK-II grew over 20% with strong domestic consumption trends. Hair Care organic sales increased high single digits led by strong demand in North America, Greater China and Latin America, with mid-single digit growth or better across each of P&G’s top hair care brands.

- Grooming segment organic sales increased six percent versus year ago. Appliances organic sales increased more than 30% due to innovation, increased demand for dry shaving and styling products, and increased pricing. Shave Care organic sales were unchanged as high single digit growth in female blades & razors was offset by market softness in male blades & razors due to pandemic-related consumption decline.

- Health Care segment organic sales increased 12% for the quarter. Oral Care organic sales increased mid-teens globally, with mid-single digit or better growth in each region driven by innovation, currency devaluation-related price increases and positive mix impacts. Personal Health Care organic sales increased high single digits primarily due to innovation and increased consumption, primarily in digestive and wellness.

- Fabric and Home Care segment organic sales increased 14% for the quarter. Fabric Care organic sales increased high single digits driven by high teens growth in the North America region through new innovations, incremental brand communication, and disproportionate growth of premium forms like laundry unit dose and fabric enhancer beads. Home Care organic sales increased more than 30% driven by increases in consumer demand for home cleaning products during the pandemic, resulting in double digit growth in every region. Dish Care, Air Care, and Surface Care each grew 20% or more.

- Baby, Feminine and Family Care segment organic sales increased four percent versus year ago. Family Care organic sales increased double digits primarily due to consumption increases driven by consumers spending more time at home during the pandemic. Feminine Care organic sales increased high single digits with innovation led growth in North America and Greater China and more than 20% growth in Adult Incontinence products. Baby Care organic sales decreased low single digits as low single digit growth in the North American region was more than offset by category contraction and increased competitive activity in other regions.

Diluted net earnings per share were $1.63, a 20% increase versus the prior year driven by the increase in net sales and an increase in operating margin. Diluted net earnings per share grew 19% versus the base period Core EPS due to non-core restructuring charges in the base period. Currency-neutral net EPS increased 22% versus the prior year core EPS.

Reported gross margin increased 170 basis points versus the prior year reported gross margin. Reported gross margin increased 140 basis points versus the prior year core gross margin due to 30 basis points of non-core restructuring charges in the base period. Unfavorable foreign exchange negatively impacted gross margin by 30 basis points. On a currency-neutral basis, reported gross margin increased 170 basis points versus the prior year core gross margin driven by 120 basis points of productivity savings, 70 basis points help from lower commodity cost, 40 basis points of pricing benefit and 20 basis points of fixed cost leverage, partially offset by 80 basis points of unfavorable product mix and other costs.

Selling, general and administrative expense (SG&A) as a percentage of sales decreased 160 basis points on a reported basis versus the prior year. SG&A as a percentage of sales decreased 170 basis points versus the prior year core SG&A due to lower non-core restructuring charges in the base period. Unfavorable foreign exchange negatively impacted SG&A by 10 basis points. On a currency-neutral basis, reported SG&A as a percentage of sales decreased 180 basis points versus the prior year core SG&A as 230 basis points of sales leverage benefit and 110 basis points of savings from overhead and marketing expenses were partially offset by 110 basis points of marketing reinvestments and 50 basis points of inflation and other impacts.

Operating profit margin increased approximately 320 basis points versus the base period reported operating margin and increased 300 basis points versus the base period core operating margin. Unfavorable foreign exchange negatively impacted operating margins by 50 basis points. On a currency-neutral basis, reported operating margin increased 350 basis points versus the prior year core operating margin, including total productivity cost savings of 230 basis points for the quarter.

Fiscal Year 2021 Guidance

P&G raised its outlook for fiscal 2021 all-in sales growth from a range of one to three percent to a range of three to four percent versus the prior fiscal year. The revised range includes an estimated one percent negative impact from foreign exchange. The Company raised its outlook for organic sales growth from a range of two to four percent to a range of four to five percent.

The Company said it now expects fiscal 2021 GAAP diluted net earnings per share growth in a range of four to nine percent versus fiscal 2020 GAAP EPS of $4.96. GAAP EPS guidance now includes non-core charges in the range of $0.15 to $0.20 per share from the early debt retirement project that was initiated earlier this month. P&G raised guidance for core earnings per share growth from a range of three to seven percent to a range of five to eight percent versus fiscal 2020 core EPS of $5.12. The Company said its current outlook includes headwinds of approximately $325 million after-tax from foreign exchange impacts and $50 million after-tax from higher freight costs. The outlook also includes an estimated $150 million after tax headwind for the combined impacts of higher interest expense and lower interest income. These headwinds should be partially offset by approximately $175 million after-tax benefit from lower commodity costs.

The Company is not able to reconcile its forward-looking non-GAAP cash flow measure without unreasonable efforts because the Company cannot predict the timing and amounts of discrete cash items, such as acquisitions, divestitures, or impairments, which could significantly impact GAAP results. The Company estimates fiscal 2021 adjusted free cash flow productivity to be around 95%.

P&G expects to pay approximately $8 billion in dividends in fiscal 2021. The Company increased its outlook for common stock repurchase from a range of $6 billion to $8 billion to a range of $7 billion to $9 billion in fiscal 2021. Combined, P&G now plans to return $15 billion to $17 billion of cash to shareholders in this fiscal year.

Forward-Looking Statements

Certain statements in this release or presentation, other than purely historical information, including estimates, projections, statements relating to our business plans, objectives, and expected operating results, and the assumptions upon which those statements are based, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements generally are identified by the words “believe,” “project,” “expect,” “anticipate,” “estimate,” “intend,” “strategy,” “future,” “opportunity,” “plan,” “may,” “should,” “will,” “would,” “will be,” “will continue,” “will likely result,” and similar expressions. Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties that may cause results to differ materially from those expressed or implied in the forward-looking statements. We undertake no obligation to update or revise publicly any forward-looking statements, whether because of new information, future events or otherwise, except to the extent required by law.

Risks and uncertainties to which our forward-looking statements are subject include, without limitation: (1) the ability to successfully manage global financial risks, including foreign currency fluctuations, currency exchange or pricing controls and localized volatility; (2) the ability to successfully manage local, regional or global economic volatility, including reduced market growth rates, and to generate sufficient income and cash flow to allow the Company to affect the expected share repurchases and dividend payments; (3) the ability to manage disruptions in credit markets or changes to our credit rating; (4) the ability to maintain key manufacturing and supply arrangements (including execution of supply chain optimizations and sole supplier and sole manufacturing plant arrangements) and to manage disruption of business due to factors outside of our control, such as natural disasters, acts of war or terrorism, or disease outbreaks; (5) the ability to successfully manage cost fluctuations and pressures, including prices of commodities and raw materials, and costs of labor, transportation, energy, pension and healthcare; (6) the ability to stay on the leading edge of innovation, obtain necessary intellectual property protections and successfully respond to changing consumer habits and technological advances attained by, and patents granted to, competitors; (7) the ability to compete with our local and global competitors in new and existing sales channels, including by successfully responding to competitive factors such as prices, promotional incentives and trade terms for products; (8) the ability to manage and maintain key customer relationships; (9) the ability to protect our reputation and brand equity by successfully managing real or perceived issues, including concerns about safety, quality, ingredients, efficacy or similar matters that may arise; (10) the ability to successfully manage the financial, legal, reputational and operational risk associated with third-party relationships, such as our suppliers, contract manufacturers, distributors, contractors and external business partners; (11) the ability to rely on and maintain key company and third party information and operational technology systems, networks and services, and maintain the security and functionality of such systems, networks and services and the data contained therein; (12) the ability to successfully manage uncertainties related to changing political conditions (including the United Kingdom’s exit from the European Union) and potential implications such as exchange rate fluctuations and market contraction; (13) the ability to successfully manage regulatory and legal requirements and matters (including, without limitation, those laws and regulations involving product liability, product and packaging composition, intellectual property, labor and employment, antitrust, data protection, tax, environmental, and accounting and financial reporting) and to resolve pending matters within current estimates; (14) the ability to manage changes in applicable tax laws and regulations including maintaining our intended tax treatment of divestiture transactions; (15) the ability to successfully manage our ongoing acquisition, divestiture and joint venture activities, in each case to achieve the Company’s overall business strategy and financial objectives, without impacting the delivery of base business objectives; (16) the ability to successfully achieve productivity improvements and cost savings and manage ongoing organizational changes, while successfully identifying, developing and retaining key employees, including in key growth markets where the availability of skilled or experienced employees may be limited; and (17) the ability to successfully manage the demand, supply, and operational challenges associated with a disease outbreak, including epidemics, pandemics, or similar widespread public health concerns (including the novel coronavirus, COVID-19, outbreak). For additional information concerning factors that could cause actual results and events to differ materially from those projected herein, please refer to our most recent 10-K/A, 10-Q and 8-K reports.

About Procter & Gamble

P&G serves consumers around the world with one of the strongest portfolios of trusted, quality, leadership brands, including Always®, Ambi Pur®, Ariel®, Bounty®, Charmin®, Crest®, Dawn®, Downy®, Fairy®, Febreze®, Gain®, Gillette®, Head & Shoulders®, Lenor®, Olay®, Oral-B®, Pampers®, Pantene®, SK-II®, Tide®, Vicks®, and Whisper®. The P&G community includes operations in approximately 70 countries worldwide. Please visit http://www.pg.com for the latest news and information about P&G and its brands.

THE PROCTER & GAMBLE COMPANY AND SUBSIDIARIES

(Amounts in Millions Except Per Share Amounts)

Consolidated Earnings Information

(1) Basic net earnings per share and Diluted net earnings per share are calculated on Net earnings attributable to Procter & Gamble.

THE PROCTER & GAMBLE COMPANY AND SUBSIDIARIES

(Amounts in Millions)

Consolidated Earnings Information

(1) Net sales percentage changes are approximations based on quantitative formulas that are consistently applied.

(2) Other includes the sales mix impact from acquisitions and divestitures and rounding impacts necessary to reconcile volume to net sales.

THE PROCTER & GAMBLE COMPANY AND SUBSIDIARIES

(Amounts in Millions Except Per Share Amounts)

Consolidated Statements of Cash Flows

THE PROCTER & GAMBLE COMPANY AND SUBSIDIARIES

(Amounts in Millions Except Per Share Amounts)

Condensed Consolidated Balance Sheets

The Procter & Gamble Company

Exhibit 1: Non-GAAP Measures

The following provides definitions of the non-GAAP measures used in Procter & Gamble’s October 20, 2020 earnings release and the reconciliation to the most closely related GAAP measures. We believe that these measures provide useful perspective on underlying business results and trends (i.e., trends excluding non-recurring or unusual items) and provide a supplemental measure of year-on-year results. The non-GAAP measures described below are used by management in making operating decisions, allocating financial resources and for business strategy purposes. These measures may be useful to investors as they provide supplemental information about business performance and provide investors a view of our business results through the eyes of management. These measures are also used to evaluate senior management and are a factor in determining their at-risk compensation. These non-GAAP measures are not intended to be considered by the user in place of the related GAAP measure, but rather as supplemental information to our business results. These non-GAAP measures may not be the same as similar measures used by other companies due to possible differences in method and in the items or events being adjusted.

The Core earnings measures included in the following reconciliation tables refer to the equivalent GAAP measures adjusted as applicable for the following item:

Incremental Restructuring: The Company has historically had an ongoing level of restructuring activities. Such activities have resulted in ongoing annual restructuring related charges of approximately $250 – $500 million before tax. Since 2012, the Company has had a strategic productivity and cost savings initiative that resulted in incremental restructuring charges. The adjustment to Core earnings includes only the restructuring costs above what we believe are the normal recurring level of restructuring costs. In fiscal 2021 and onwards, the Company expects to incur restructuring costs within our historical ongoing level.

We do not view the above item to be part of our sustainable results and its exclusion from Core earnings measures provides a more comparable measure of year-on-year results. This item is also excluded when evaluating senior management in determining their at-risk compensation.

Organic sales growth: Organic sales growth is a non-GAAP measure of sales growth excluding the impacts of acquisitions and divestitures and foreign exchange from year-over-year comparisons. We believe this measure provides investors with a supplemental understanding of underlying sales trends by providing sales growth on a consistent basis. This measure is used in assessing achievement of management goals for at-risk compensation.

Core operating profit margin: Core operating profit margin is a measure of the Company’s operating margin adjusted for items as indicated. Management believes this non-GAAP measure provides a supplemental perspective to the Company’s operating efficiency over time.

Core gross margin: Core gross margin is a measure of the Company’s gross margin adjusted for items as indicated. Management believes this non-GAAP measure provides a supplemental perspective to the Company’s operating efficiency over time.

Core selling, general and administrative (SG&A) expense as a percentage of net sales: Core SG&A expense as a percentage of net sales is a measure of the Company’s selling, general and administrative expenses adjusted for items as indicated. Management believes this non-GAAP measure provides a supplemental perspective to the Company’s operating efficiency over time.

Core EPS: Core earnings per share, or Core EPS, is a measure of the Company’s diluted net earnings per share adjusted as indicated. Management views this non-GAAP measure as a useful supplemental measure of Company performance over time. This measure is also used when evaluating senior management in determining their at-risk compensation.

Currency-neutral net EPS growth: Currency-neutral net EPS growth is a measure of the Company’s EPS growth versus the prior period Core EPS excluding the incremental current year impact of foreign exchange. Management views this non-GAAP measure as useful supplemental measures of Company performance over time.

Adjusted free cash flow: Adjusted free cash flow is defined as operating cash flow less capital spending and adjustment for the transitional tax resulting from the U.S. Tax Act (the Company incurred a transitional tax liability of approximately $3.8 billion from the U.S. Tax Act, which is payable over a period of 8 years). Adjusted free cash flow represents the cash that the Company is able to generate after taking into account planned maintenance and asset expansion. Management views adjusted free cash flow as an important measure because it is one factor used in determining the amount of cash available for dividends, share repurchases, acquisitions and other discretionary investments.

Adjusted free cash flow productivity: Adjusted free cash flow productivity is defined as the ratio of adjusted free cash flow to net earnings. Management views adjusted free cash flow productivity as a useful measure to help investors understand P&G’s ability to generate cash. Adjusted free cash flow productivity is used by management in making operating decisions, allocating financial resources and for budget planning purposes. This measure is also used in assessing the achievement of management goals for at-risk compensation. The Company’s long-term target is to generate annual adjusted free cash flow productivity at or above 90 percent.

THE PROCTER & GAMBLE COMPANY AND SUBSIDIARIES

(Amounts in Millions Except Per Share Amounts)

Reconciliation of Non-GAAP Measures

(1) Diluted net earnings per share are calculated on Net earnings attributable to Procter & Gamble.

(2) While total restructuring costs exceeded the historical ongoing level, total restructuring costs included within SG&A for this period were below the historical ongoing level. Accordingly, the non-GAAP adjustment for the SG&A line item adds costs to the comparable GAAP number.

(1) Change versus year ago is calculated based on As Reported (GAAP) values for the three months ended September 30, 2020 versus the Non-GAAP (Core) values for the three months ended September 30, 2019.

Organic sales growth:

(1) Includes rounding impacts necessary to reconcile net sales to organic sales.

(1) Includes rounding impacts necessary to reconcile net sales to organic sales.

Core EPS growth:

(1) Includes impact of prior year incremental non-core restructuring charges and early debt extinguishment charges expected in FY2021.

Adjusted free cash flow (dollar amounts in millions):

Adjusted free cash flow productivity (dollar amounts in millions):

View source version on businesswire.com: https://www.businesswire.com/news/home/20201020005617/en/