Tissue news: structural challenges in the US, China growth, DTC insurgency

With positive growth recorded in volume and value globally, the consumer tissue industry has something to feel optimistic about. Furthermore, easing of pulp prices and the ability of some manufacturers to implement retail price increases are complemented by a still significant global unmet potential for consumer tissue, estimated at over 17 million tonnes, or over USD 51 billion, in incremental sales.

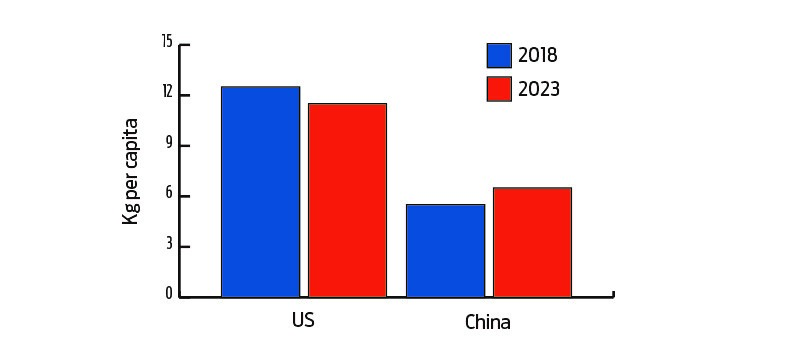

China and the US remain the world’s two largest retail consumer tissue markets, by volume and value, together accounting for nearly half of all global consumer tissue sales in 2018. However, while the US continues to struggle with significant structural challenges, China sees healthy projections ahead.

In the US, in volume terms, the retail market saw a decline in 2018, and it is projected to remain largely in negative territory over the next five years. As key macro-fundamentals shape demand and retail sales, slowing economic projections and persistent low levels of population growth (well under 1% annually) will continue to impact the industry. Furthermore, the Euromonitor Industry Forecasting model predicts that US-China trade wars are likely to shave some growth off going forward. While the downgrade in projections due to trade wars is not likely to be significant, any further slowdown in an already sluggish market is not good news. Trade wars can and likely will lead to further increases in prices in retail across consumer goods, in addition to price increases already implemented in 2018, thereby forcing many consumers to re-evaluate their spending priorities and giving cheaper brands and an already strong private label an upper hand once again. Euromonitor consumer lifestyle surveys reveal that many consumers in the US intend to increase their spending in discounters and spend more on private label in 2019.

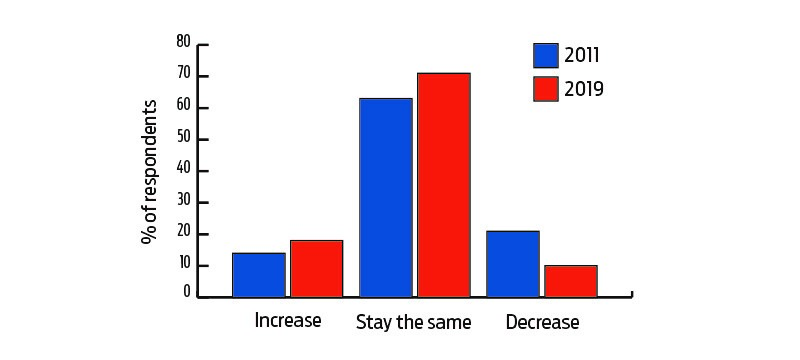

In fact, the proportion of US respondents planning to increase their spending on private label in the coming 12 months went up from 14% in the 2011 survey to 17% in the 2017 survey to 19% in the 2019 survey.

China is expected to add another two million plus tonnes in incremental retail sales of consumer tissue

This is not to say that all is doom and gloom for the key industry suppliers and brands in the US. Products that provide tangible benefits to consumers always have their place in households. Thus, for instance, paper towels in the US saw a somewhat better performance in 2018, compared to the previous year. While price increases implemented by key brands and fewer promotions did play a role in boosting nominal value upwards, product positioning and improvements in quality and strength also continue to support the category.

On the other hand, China’s consumer tissue market has seen remarkable growth in the past few years and is expected to record healthy gains in volume and value in the next five years. While the market already features high retail per capita consumption of facial tissue, retail per capita in other consumer tissue categories still leaves significant room for further organic growth. Thus, retail consumption of toilet paper remains at less than a half of the per capita in North America and Western Europe, and paper towels and paper tableware categories are even less developed. All in all, over 2018-2023, China is expected to add another two million plus tonnes in incremental retail sales of consumer tissue, or an estimated USD 6 billion. Importantly, as the country’s unmet potential in consumer tissue is estimated at over four million tonnes, or USD 11 billion, there remains significant room for further organic industry growth in the country, well beyond 2023.

Higher purchasing power, coupled with rising modern hygiene and product awareness, afford Chinese consumers, especially those from rural areas, increased usage frequency of tissue products. While toilet paper still accounts for over half of total retail tissue volume in China, its relative share has been shrinking, as boxed facial tissues and paper towels have been gaining momentum.

On the competitive side, private label accounts for a tiny portion of retail tissue sales in China, and the market remains open to value-added and premium innovation. Additionally, as online sales in China continue to see strong growth, new competition in the form of direct-to-consumer tissue brands is emerging across both value and premium segments. Surging online space also supports the survival and the evolution of a number of brands that face challenges from the new policies implemented in the country. Pressured by strict government policies on environmental protection, small mills and manufacturers that failed to reach national standards have been forced to shut down. However, a number of online players, notably Botare owned by Fujian Duoduoyun, not only survived but are in fact thriving, thanks to the rise of social commerce giant Pinduoduo and with the help of Lee & Man Paper’s industrial clusters park in Jiangxi. Companies inside the park get paper from Lee & Man directly and then package and sell only a small number of SKUs. This business model allows the brands to radically reduce the cost as well as transportation time. Subsequently, the products are competitively priced without compromising much on quality, offer consumers a new value-for-money choice, and gain a substantial online presence in a rapidly growing digital retail. Euromonitor consumer lifestyle surveys indicated that while Chinese consumers do not necessarily place low price at the top of their priority list when it comes to shopping for household essentials, value-for-money is an important feature for nearly 39% of consumers, followed closely by high quality of products. Low price has been selected as an important feature by only 10% of respondents in China. By comparison, 43% of US respondents indicated low price as an important feature and 50% indicated value for money. As Chinese consumers evolve, get more familiar with products, get access to more brands and retail/pricing options, they will likely to rationalize their purchases more.

Value-for-money, therefore, is likely to stay high and potentially increase further on the priority list for consumer shopping for household essentials. Hence, while China indeed offers a significant potential for long-term growth, it is crucial to understand the evolution of consumer needs and priorities as they get wider exposure for a variety of consumer tissue products and to respond accordingly when it comes to innovation, marketing, and retail strategies.