P&G Announces Fiscal Year 2021 Second Quarter Results

The company reported second quarter fiscal year 2021 net sales of $19.7 billion, an increase of eight percent versus the prior year.

The Procter & Gamble Company reported second quarter fiscal year 2021 net sales of $19.7 billion, an increase of eight percent versus the prior year. Excluding the net impacts of foreign exchange, acquisitions and divestitures, organic sales also increased eight percent. Diluted net earnings per share were $1.47, an increase of four percent versus the prior year. Core EPS was $1.64, an increase of 15% versus the prior year. Currency-neutral core EPS increased 18% versus the prior year.

Operating cash flow was $5.4 billion for the quarter. Adjusted free cash flow productivity was 113%. The Company returned $5 billion of cash to shareholders via $2 billion of dividend payments and $3 billion of common stock repurchases.

“We delivered another strong quarter of results across all key measures – top line, bottom line and cash,” said David Taylor, Chairman, President and Chief Executive Officer. “We remain focused on executing our strategies of superiority, productivity, constructive disruption and improving P&G’s organization and culture. These strategies enabled us to build strong business momentum before the COVID crisis, accelerated our progress in calendar year 2020 and remain the right strategies to deliver balanced growth and value creation over the long term.”

OCTOBER – DECEMBER QUARTER DISCUSSION

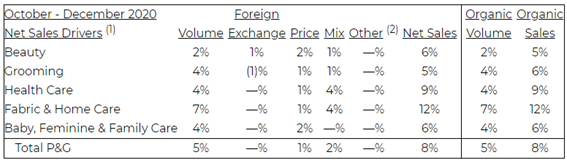

Net sales in the second quarter of fiscal year 2021 were $19.7 billion, an eight percent increase versus the prior year. Organic sales, which excludes the impacts of foreign exchange, acquisitions and divestitures, also increased eight percent, driven by a five percent increase in shipment volume, one percentage point of increased pricing and two percentage points of positive mix impact. Positive mix was driven by the disproportionate growth of the higher-priced Home Care and Appliances categories and the North America region. Foreign exchange had no net impact to net sales for the quarter.

(1) Net sales percentage changes are approximations based on quantitative formulas that are consistently applied.

(2) Other includes the sales mix impact from acquisitions and divestitures and rounding impacts necessary to reconcile volume to net sales.

- Beauty segment organic sales increased five percent versus year ago. Skin and Personal Care organic sales increased mid-single digits primarily driven by innovation, increased pricing and positive mix impact of premium Olay Skin Care and Safeguard hand soap and hand sanitizer launches. Hair Care organic sales increased mid-single digits led by strong demand and retail execution in Greater China and increased pricing.

- Grooming segment organic sales increased six percent versus year ago. Appliances organic sales increased more than 20% due to increased demand for at-home shaving and styling products and innovation. Shave Care organic sales increased low single digits driven by innovation and devaluation-related pricing, partially offset by category contraction due to the pandemic and negative geographic mix impact.

- Health Care segment organic sales increased nine percent for the quarter. Oral Care organic sales increased double digits, with high single digits or higher growth in each region driven by innovation and positive mix impacts from the disproportionate growth of premium products. Personal Health Care organic sales increased mid-single digits primarily due to innovation, increased consumption, and increased pricing, partially offset by negative mix due to a decline in the sales of respiratory products driven by a lower than average incidence of cough, cold and flu this season.

- Fabric and Home Care segment organic sales increased 12% for the quarter. Fabric Care organic sales increased high single digits driven by innovations, incremental marketing spending, the disproportionate growth of premium forms like laundry unit dose and fabric enhancer beads and increased pricing. Home Care organic sales increased around 30% driven by increased consumer demand for home cleaning products during the pandemic, premium innovation and incremental marketing spending resulting in mid-single digits or higher growth in every region. Dish Care, Air Care and Surface Care each grew high teens or more.

- Baby, Feminine and Family Care segment organic sales increased six percent versus year ago. Baby Care organic sales increased low single digits primarily driven by mid-single digit growth in North America and devaluation-related price increases in certain regions, partially offset by category contraction in certain regions due to the pandemic and competitive activity. Feminine Care organic sales increased mid-single digits driven by positive product mix due to premium innovation growth in North America and Greater China and devaluation-related price increases in certain regions. Family Care organic sales increased double digits driven by consumption increases as consumers spend more time at home during the pandemic.

- Diluted net earnings per share were $1.47, a four percent increase versus the prior year driven by the increase in net sales and an increase in operating margin, partially offset by charges for early debt extinguishment in the current period. Core earnings per share were $1.64, a 15% increase versus the prior year driven primarily by the increase in net sales and operating margin. Currency-neutral core earnings per share increased 18% for the quarter.

Diluted net earnings per share were $1.47, a four percent increase versus the prior year driven by the increase in net sales and an increase in operating margin, partially offset by charges for early debt extinguishment in the current period. Core earnings per share were $1.64, a 15% increase versus the prior year driven primarily by the increase in net sales and operating margin. Currency-neutral core earnings per share increased 18% for the quarter.

Reported gross margin increased 170 basis points versus the prior year reported gross margin. Reported gross margin increased 150 basis points versus the prior year core gross margin due to 20 basis points of non-core restructuring charges in the base period. Unfavorable foreign exchange negatively impacted gross margin by 50 basis points. On a currency-neutral basis, reported gross margin increased 200 basis points versus the prior year core gross margin driven by 180 basis points of productivity savings, 70 basis points of benefit from increased pricing and 30 basis points help from lower commodity costs, partially offset by 80 basis points of unfavorable product mix and other costs. Productivity savings include approximately 20 basis points of headwind from freight cost increases.

Selling, general and administrative expense (SG&A) as a percentage of sales decreased 90 basis points on a reported basis versus the prior year. SG&A as a percentage of sales decreased 100 basis points versus the prior year core SG&A due to lower non-core restructuring charges in the base period. Unfavorable foreign exchange negatively impacted SG&A by 10 basis points. On a currency-neutral basis, reported SG&A as a percentage of sales decreased 110 basis points versus the prior year core SG&A as 210 basis points of sales leverage benefit and 100 basis points of productivity savings from overhead and marketing expenses were partially offset by approximately 120 basis points of marketing reinvestments and approximately 80 basis points of inflation and other impacts.

Operating profit margin increased 260 basis points versus the base period reported operating margin. Operating profit margin increased 250 basis points versus the base period core operating margin due to 10 basis points of non-core restructuring charges in the base period. Unfavorable foreign exchange negatively impacted operating margins by approximately 60 basis points. On a currency-neutral basis, reported operating margin increased 310 basis points versus the prior year core operating margin, including total productivity cost savings of 280 basis points for the quarter.

FISCAL YEAR 2021 GUIDANCE

P&G raised its outlook for fiscal 2021 all-in sales growth from a range of three to four percent to a range of five to six percent versus the prior fiscal year. The Company raised its outlook for organic sales growth from a range of four to five percent to a range of five to six percent. Foreign exchange is now expected to be roughly neutral to sales growth for the fiscal year.

The Company said it now expects fiscal 2021 GAAP diluted net earnings per share growth in the range of eight to ten percent versus fiscal 2020 GAAP EPS of $4.96. GAAP EPS guidance includes non-core charges for early debt retirement of $0.16 per share in fiscal 2021. P&G raised guidance for core earnings per share growth from a range of five to eight percent to a range of eight to ten percent versus fiscal 2020 core EPS of $5.12. The Company said its current outlook includes headwinds of approximately $100 million after-tax from foreign exchange impacts and $100 million after-tax from higher freight costs. The outlook also includes an estimated $150 million after tax headwind for the combined impacts of higher interest expense and lower interest income. The Company now expects commodity cost impact to be neutral versus the previous fiscal year.

The Company is not able to reconcile its forward-looking non-GAAP cash flow measure without unreasonable efforts because the Company cannot predict the timing and amounts of discrete cash items, such as acquisitions, divestitures, or impairments, which could significantly impact GAAP results. The Company now estimates fiscal 2021 adjusted free cash flow productivity to be in the range of 95% to 100%.

P&G expects to pay approximately $8 billion in dividends in fiscal 2021. The Company increased its outlook for common stock repurchase from a range of $7 billion to $9 billion to up to $10 billion in fiscal 2021. Combined, P&G now plans to return around $18 billion of cash to shareowners in this fiscal year.

FORWARD-LOOKING STATEMENTS

Certain statements in this release or presentation, other than purely historical information, including estimates, projections, statements relating to our business plans, objectives, and expected operating results, and the assumptions upon which those statements are based, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements generally are identified by the words “believe,” “project,” “expect,” “anticipate,” “estimate,” “intend,” “strategy,” “future,” “opportunity,” “plan,” “may,” “should,” “will,” “would,” “will be,” “will continue,” “will likely result,” and similar expressions. Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties that may cause results to differ materially from those expressed or implied in the forward-looking statements. We undertake no obligation to update or revise publicly any forward-looking statements, whether because of new information, future events or otherwise, except to the extent required by law.

Risks and uncertainties to which our forward-looking statements are subject include, without limitation: (1) the ability to successfully manage global financial risks, including foreign currency fluctuations, currency exchange or pricing controls and localized volatility; (2) the ability to successfully manage local, regional or global economic volatility, including reduced market growth rates, and to generate sufficient income and cash flow to allow the Company to affect the expected share repurchases and dividend payments; (3) the ability to manage disruptions in credit markets or changes to our credit rating; (4) the ability to maintain key manufacturing and supply arrangements (including execution of supply chain optimizations and sole supplier and sole manufacturing plant arrangements) and to manage disruption of business due to factors outside of our control, such as natural disasters, acts of war or terrorism, or disease outbreaks; (5) the ability to successfully manage cost fluctuations and pressures, including prices of commodities and raw materials, and costs of labor, transportation, energy, pension and healthcare; (6) the ability to stay on the leading edge of innovation, obtain necessary intellectual property protections and successfully respond to changing consumer habits and technological advances attained by, and patents granted to, competitors; (7) the ability to compete with our local and global competitors in new and existing sales channels, including by successfully responding to competitive factors such as prices, promotional incentives and trade terms for products; (8) the ability to manage and maintain key customer relationships; (9) the ability to protect our reputation and brand equity by successfully managing real or perceived issues, including concerns about safety, quality, ingredients, efficacy or similar matters that may arise; (10) the ability to successfully manage the financial, legal, reputational and operational risk associated with third-party relationships, such as our suppliers, contract manufacturers, distributors, contractors and external business partners; (11) the ability to rely on and maintain key company and third party information and operational technology systems, networks and services, and maintain the security and functionality of such systems, networks and services and the data contained therein; (12) the ability to successfully manage uncertainties related to changing political conditions (including the United Kingdom’s exit from the European Union) and potential implications such as exchange rate fluctuations and market contraction; (13) the ability to successfully manage regulatory and legal requirements and matters (including, without limitation, those laws and regulations involving product liability, product and packaging composition, intellectual property, labor and employment, antitrust, data protection, tax, environmental, and accounting and financial reporting) and to resolve pending matters within current estimates; (14) the ability to manage changes in applicable tax laws and regulations including maintaining our intended tax treatment of divestiture transactions; (15) the ability to successfully manage our ongoing acquisition, divestiture and joint venture activities, in each case to achieve the Company’s overall business strategy and financial objectives, without impacting the delivery of base business objectives; (16) the ability to successfully achieve productivity improvements and cost savings and manage ongoing organizational changes, while successfully identifying, developing and retaining key employees, including in key growth markets where the availability of skilled or experienced employees may be limited; and (17) the ability to successfully manage the demand, supply, and operational challenges associated with a disease outbreak, including epidemics, pandemics, or similar widespread public health concerns (including the novel coronavirus, COVID-19, outbreak). For additional information concerning factors that could cause actual results and events to differ materially from those projected herein, please refer to our most recent 10-K/A, 10-Q and 8-K reports.

For more information, tables and attachments, visit: news.pg.com/news-releases/news-details/2021/PG-Announces-Fiscal-Year-2021-Second-Quarter-Results/default.aspx.