Tissue Planet: global industry discusses a level playing field, decarbonization and the future of papermaking

Over two days of presentations in Lucca, global leaders converged on the shifts reshaping the tissue industry: Asian imports, energy cost, profitable decarbonization, AI applied to operations and the urgent need for a level playing field

Held in Lucca, the second edition of Tissue Planet, organized by Toscotec, positioned itself as a strategic forum for the global industry. Executives from European, Latin American and North American producers, machine and pulp suppliers, consultancies and academia converged on a shared diagnosis: the sector is going through a structural transformation driven by demography, geopolitics, energy cost and sustainability expectations.

CEO | Toscotec. Photo: Nexum Group

CEO Alessandro Mennucci and Sales Director Marco Dalle Piagge opened the event as a community space: “Sustainability, responsibility, AI and innovation are not separate topics, but part of the same conversation.”

Professor of Digital Ethics and Defence Technologies – Oxford Internet Institute | University of Oxford. Photo: Nexum Group

ETHICS, AI AND THE LIMITS OF DELEGATION TO MACHINES

Mariarosaria Taddeo (Oxford Internet Institute) argued that ethics is the foundation for rethinking industrial production in the age of AI. “AI is not a replacement for talent,” she said, proposing that “trust is a form of delegation without supervision; when we delegate to a machine, we forget we are still responsible.” The central risk, in her view, is not job displacement but concentration of data, infrastructure and models in few actors, with consequences for sovereignty, competition and the material cost of AI in energy, water and infrastructure.

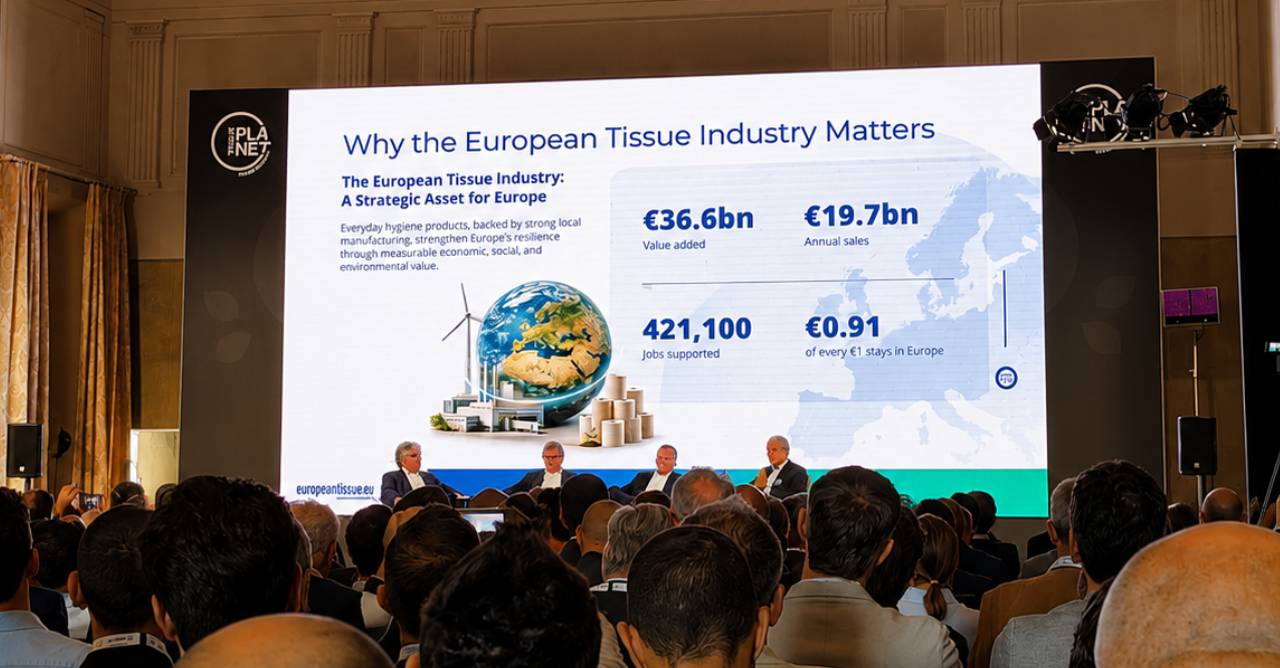

EUROPEAN TISSUE: 36.6 BILLION EUROS AND A CALL FOR REGULATORY RECIPROCITY

The European roundtable, moderated by Marco Dell’Osso (MDG35), brought together Carlos Reinoso (ETS), Martin Krengel (Wepa Group) and Volker Zöller (Essity). Reinoso presented the first comprehensive socio-economic study of the sector: European tissue generates 36.6 billion euros in added value, 19.7 billion in annual sales and sustains more than 421,000 jobs; for every 1 euro spent, 0.91 euro stays in Europe. Full migration of European public restrooms to paper towels could prevent 9.8 million flu infections per year. Zöller warned that energy costs in Europe are around 150% of those in China and 350% of those in the US: “We want fair regulation, with a level playing field for those who already comply with strict rules on sustainability, forest certification and traceability.”

“THERE WILL BE NO NEW NORMALITY”

Luigi Lazzareschi (Sofidel) offered the sharpest contrast between the two sides of the Atlantic: more than 52% of group revenue comes from the US, with two thirds of income generated there. The North American market combines no overcapacity, concentrated customer base, one language and one set of regulations; Europe is the opposite, with fragmented retailers and an industry that “installed too many machines over the last 20 years.” He rejected the idea of a “new normality” and pointed to double pressure: demographics (more than 1 million births in Italy in 1963; fewer than 400,000 last year) combined with volatility, inflation and gas costs. On Asian imports, he was emphatic: US tariffs did not close down factories in Asia, they redirected flows toward Northern Europe. He argued that EUDR, if properly implemented, would already be enough to make many unfair imports unviable.

SUSTAINABILITY AND SUPPLY CHAIN; PATH TO THE AUTONOMOUS MIL

Olli Härkönen (Essity) presented a clear diagnosis: direct operations account for around 8% of total emissions; the challenge lies in Scope 3. Since June, the company operates its first plant entirely free of fossil fuels. “We do not rely only on technology or on capital. We rely on the people who execute the strategy every day.” Next, Andreas Endters (Voith Paper) presented the next generation of the technology, capable of operating with 95% less water and more than 20% less energy, and the MillOne suite, developed with IBM, applying AI on top of the data layer (“Data Arc”). Around 1,200 recognition and monitoring systems are already running in the field, with efficiency gains between 10% and 20%, supported by four data centers, one on each continent.

Consumer Goods Executive Vice President | Suzano. Photo: Nexum Group.

GLOBAL VIEW AND THE LATIN AMERICAN OPPORTUNITY

Luís Bueno (Suzano) opened day two: tissue is a USD 48 billion market growing at 3% per year, with China and the US accounting for half of demand under opposite dynamics. China is expanding capacity faster than demand, redirecting surplus to Southeast Asia, Australia and Latin America, and advancing in pulp verticalization. On Europe, he highlighted concentrated capacity, energy and logistics as disadvantages, mounting import pressure and sustainability as a competitive differentiator. On Latin America, he read opportunity: a consolidated market, low penetration of categories beyond bath tissue and clear quality trade-up potential. In Brazil, per capita consumption ranges from 5 kg/year in São Paulo to 2-3 kg/year in the North and Northeast, 90% of the market is bath tissue (versus 60% globally), and the pricing scenario is one of the worst in the world.

Executive Director | The Navigator Company. Photo: Nexum Group.

INTEGRATED DECARBONIZATION AND FURNISH OPTIMIZATION

Nuno Santos (The Navigator Company) detailed the Portuguese company’s commitments, integrated from forest to finished product: 86% reduction in ETS emissions by 2035 (42% already delivered), 63% in Scope 1 and 2 and 30.5% in Scope 3. Among 20 Iberian and French tissue producers, it delivers the finished product with the lowest emissions footprint (FisherSolve). He presented four concrete actions: a steam turbine fed by biomass boilers, a new biomass boiler in Vila Velha de Ródão replacing natural gas, steam boosters and rooftop solar plants. “Every investment must have a positive IRR.” Darryl Holt (UPM Pulp) added that tissue is the only paper segment growing toward 2040 (around 8 million additional tonnes globally), while pulp capacity additions over the last 10 to 15 years have been dominated by hardwood, making softwood progressively scarcer. In a TAD pilot, softwood content dropped from 60% to 35% while preserving all key metrics, with savings of 8.5% per tonne; at industrial scale, 50% of softwood was replaced with birch in a kitchen towel grade.

VP Sustainability & Corporate Communications | Kruger Products. Photo: Nexum Group.

OPERATIONAL ESG, PROFITABLE NET-ZERO AND INTEGRATED DESIGN

Steven Sage (Kruger Products) presented Reimagine 2030: 31% emissions reduction (target 35%), 40% water intensity reduction (target raised to 45%) and 90% of fiber already FSC certified. He highlighted that sustainability has shifted from baseline to differentiator and that the sector suffers from overuse of generic claims (“eco,” “green,” “natural”) that generate mistrust. Eduardo de Almeida (AFRY) argued that well-designed decarbonization improves profitability: in cases analyzed, projects reach 50% decarbonization with IRR above baseline, with a steep curve and site-by-site design, citing Spain as a glimpse of the future of European grids. Peter Oksakowski (BHM INGENIEURE) reminded the audience that around 50% of the capex of a new mill goes into buildings and infrastructure, and that integrated design can deliver up to 20% capex reduction, up to 25% opex savings and up to 40% in life-cycle cost. “Process and intralogistics must drive layout, not the other way around.”

EUROPEAN INDUSTRIAL HERITAGE AND THE SCENARIO TO 2040

Elena Troia (EuroVast) offered a provocative reading of ESG, starting with governance, then social and only then environment. The family company operates 10 sites across Italy, the United Kingdom and the Netherlands, and built its trajectory through patient recovery of five mills that had been shut down; it installed the first eYMP (electric Yankee with metal jacket) in the world and has a science-based target to reduce Scope 1 and 2 by 42% in ten years. Closing the event, Philipp Jaki (Fastmarkets) provided the macro picture: Europe will turn to negative population growth in 2026 and relies on natural gas for around 84% of tissue production; Asian imports to Europe rose from 142,000 tonnes in 2022 to around 340,000 in 2025, while the Asia-Europe production cost gap widened to USD 300 per tonne and 40-foot container freight dropped from over USD 10,000 to USD 3,000. His recommendation: label product origin clearly and reposition storytelling around origin and sustainability. By 2040, China and North America will account for around half of global consumption; China will remain the main driver of volume growth.

AN INDUSTRY THAT HAS TO DECIDE TOGETHER

Tissue Planet 2026 made it clear that Asian imports, energy, profitable decarbonization, AI applied to operations, supply chain integrity and asymmetric regulation can no longer be addressed in isolation. Speakers converged on three points: the need for a level competitive playing field with effective enforcement of existing European rules (EUDR, ETS); decarbonization as a vector of competitiveness, with concrete cases of positive IRR; and the role of people and governance as a central condition. For the Latin American industry, the reading is one of opportunity: while Europe and Asia face a pressured board, the region stands out as a space of genuine growth, with quality trade-up potential, low penetration of categories beyond bath tissue and efficiency and decarbonization gains still to be unlocked.